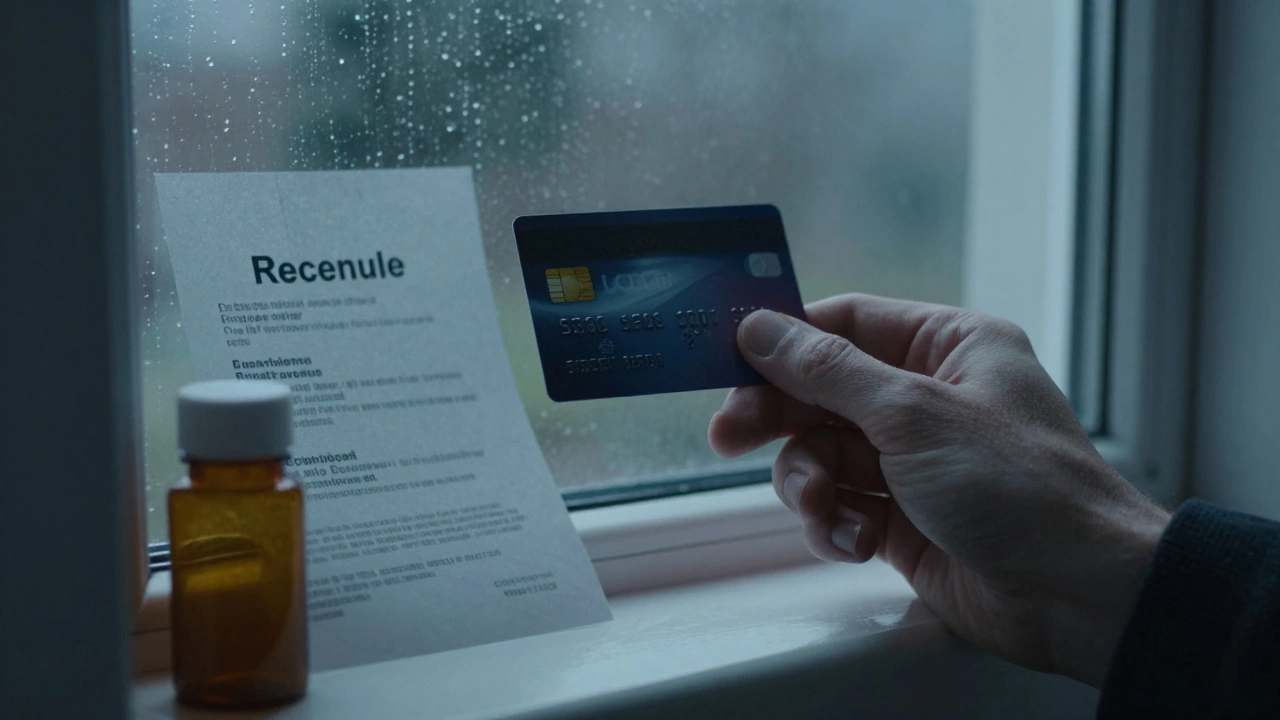

Bank accounts get frozen. Payment processors shut down. Credit cards are declined-without warning, without explanation. For sex workers, this isn’t an anomaly. It’s the norm. Financial discrimination isn’t just inconvenient; it’s life-threatening. When you can’t pay rent, buy groceries, or access emergency care because your bank decided your work is too risky, you’re not just being inconvenienced-you’re being erased from the economy. This isn’t about morality. It’s about survival. And it’s happening right now, in cities from London to Perth, to people who are already marginalized.

Some sex workers turn to informal networks to survive. Others rely on cash. But cash is dangerous. It’s harder to track, harder to save, and easier to steal. A few even use services like best london escort agency to manage client payments through third-party platforms that don’t ask invasive questions. These aren’t loopholes-they’re workarounds built out of necessity. And they highlight a brutal truth: the financial system isn’t broken for sex workers. It was designed this way.

How Banks Decide Who Deserves Access

Banks don’t have a public list of banned professions. But they have internal risk algorithms that flag certain keywords: "escort," "cam model," "adult entertainment," "private sessions." These triggers automatically escalate accounts for review. Sometimes, the account is closed. Other times, the client is asked to provide "proof of legitimate income"-a request no teacher, nurse, or software developer ever gets.

These policies aren’t based on crime. They’re based on stigma. A 2023 study by the Global Network of Sex Work Projects found that 78% of sex workers in high-income countries had experienced bank account closures. In the UK alone, over 2,000 accounts were shut down between 2020 and 2023 under "financial crime prevention" guidelines. Not one of those closures led to a criminal conviction.

Meanwhile, banks openly serve industries with far higher risks of fraud and exploitation-online gambling, crypto trading, even payday lenders. But sex work? That’s "high risk." Why? Because of outdated laws, moral panic, and the assumption that sex work is inherently illegal or exploitative. It’s not. In many places, including parts of Australia, sex work is legal. But banking laws haven’t caught up.

The Ripple Effect: Housing, Healthcare, and Safety

When you can’t open a bank account, you can’t get a lease. Landlords run credit checks. No bank history? No rental. You’re pushed into unsafe housing-or homelessness. In Sydney, a 2024 survey by the Scarlet Alliance found that 41% of sex workers had been evicted or denied housing in the past year because of their income source.

Healthcare is another casualty. Many clinics require direct debit for appointments. Without a bank account, you can’t schedule a regular STI test. No insurance? No prescription refills. In London, a sex worker interviewed by the English Collective of Prostitutes said she skipped her HIV medication for three months because her card was declined at the pharmacy. She didn’t report it. She didn’t trust the system.

And when emergencies happen-assault, violence, medical crisis-you can’t call for help without proof of identity or address. Police often refuse to file reports if they see "escort" listed as an occupation. Banks have made it impossible to prove you’re a legitimate worker. So you stay silent. And the cycle continues.

How the System Targets Women and Trans People Most Harshly

Financial discrimination doesn’t affect everyone equally. Women, trans people, migrants, and people of color face the harshest penalties. A trans sex worker in Melbourne was denied a loan to start her own business because the bank said her ID didn’t "match" her occupation. A migrant sex worker in London lost her savings when her remittance app flagged her transactions as "suspicious."

These aren’t edge cases. They’re systemic. Financial institutions rely on outdated gender norms and racial profiling. A man working as a male escort is far less likely to be flagged than a woman doing the same job. A Black trans woman is three times more likely to have her account closed than a white cisgender man in the same profession.

Even when laws change, banking policies don’t. The decriminalization of sex work in New Zealand in 2003 didn’t lead to better banking access. In Canada, after partial decriminalization in 2014, banks still refused to serve sex workers. Legal reform without financial inclusion is empty.

What’s Being Done-And Who’s Leading the Change

Organizations like the Global Network of Sex Work Projects and the English Collective of Prostitutes are pushing for financial inclusion policies. In Australia, the Sex Workers Outreach Project (SWOP) has trained bank staff in Perth and Adelaide to recognize legitimate income from sex work. Some credit unions now offer accounts with no occupation-based restrictions.

There are also fintech startups building alternatives. Platforms like PayMyWorker and SafePay allow sex workers to receive payments without needing a traditional bank. These services don’t ask for proof of employment. They don’t flag "escort" as a red flag. They just process payments. One user in London said, "For the first time, I can pay my bills without hiding my work."

But these tools are still niche. Most sex workers don’t know they exist. And they’re not backed by government support. Without policy change, these are temporary fixes-not solutions.

What You Can Do-Even If You’re Not a Sex Worker

You don’t have to be a sex worker to fight financial discrimination. Here’s what actually helps:

- Support organizations that advocate for sex worker rights, like SWOP or the Global Network of Sex Work Projects.

- Ask your bank: Do you have a policy on serving sex workers? If not, demand one.

- Use services that don’t discriminate. If you’re hiring an escort, pay through platforms that protect worker privacy.

- Amplify sex worker voices. Share their stories. Don’t speak for them-listen.

- Vote for politicians who support decriminalization and financial inclusion. This isn’t a fringe issue. It’s an economic justice issue.

There’s a myth that this is about protecting people from exploitation. But the real exploitation is being locked out of the economy because of who you are and what you do. The solution isn’t to shame or criminalize. It’s to include.

Why This Matters Beyond Sex Work

This isn’t just about sex workers. It’s about who gets to be seen as worthy in our economy. If banks can shut down accounts based on occupation alone, what’s next? Freelancers? Gig workers? Artists? People with criminal records? The same algorithms that block sex workers are being used to deny loans to immigrants, reject applications from people in low-income neighborhoods, and freeze accounts of activists.

Financial exclusion is a tool of control. And once you accept that one group doesn’t deserve access, you open the door for it to be used against anyone.

Sex workers aren’t asking for special treatment. They’re asking for the same rights everyone else has: to bank, to rent, to get healthcare, to live without fear. That’s not radical. It’s basic.

And if you can’t see that, maybe you’re not seeing the whole picture.